Merchant Accounts

Where to get a Merchant Account for your Online Business

This post is a continuation of the previous, Where to incorporate as a Digital Nomad, where we continue to explore options for internet entrepreneurs to successfully structure their business. In that article, we talked about the importance of having a legal entity but didn’t touch on bank accounts (coming next) or merchant accounts.

In this article, I will show how you can structure your company with a merchant account or payment processor to accept credit card payments via the web. You could call this article: Where to get a merchant account for my online business. If you want to skip all this and just have us help you get an account, use the form below.

First, a quick overview of terms.

- Gateways – refer to the front-end, storefront or shopping cart which captures and passes credit card information along to the payment processor merchant account (either of which may provide their own gateway).

- Payment Processors – refers to the “full stack, end-to-end solution” that companies like Stripe, Paypal provide to their customers

- Merchant Accounts (through merchant banks) – refer to the provider that charges the credit card, that has an agreement with credit card companies, and resell their solutions to merchants.

Now will break down 4 different scenarios,

Part 1: Deals with onshore merchant accounts (within the USA) where the merchant account and payment processing ecosystem is the most developed.

Part 2: Talks about the UK system, as well as a 0% tax option for operating with a merchant account in G.B.

Part 3: Discusses offshore merchant accounts. Why you might want to explore this as an option, and what to expect.

Part 4: Presents options for higher risk accounts and alternative payment systems.

Part 1: Onshore

USA Banking

It is very possible that you could have great benefits from a simple set up within the United States. This is because banking in the USA offers some distinct advantages. Being the world’s largest economy (at the time of publication) the US also has the most advanced banking system and one that does provide some simple benefits to startups and SMEs. There are many different options in terms of credit card processing, and this might be a good place to look first if you are looking to process payments online.

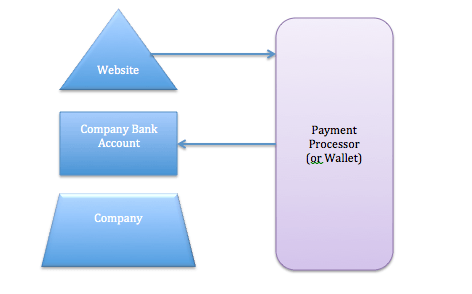

Many businesses get great use out of selling on Amazon or hooking up to a Silicon Valley giant like Paypal or Stripe, simply because these platforms make payments very easy. As shown on the diagram below, the payment processor (which is a full stack solution such as Paypal) provides the gateway and the merchant account. They often secure their own, independent relationships with the bank. Therefore, it is difficult to negotiate any sort of preferential terms. However, one doesn’t need to know anything about payments to get started. Great for beginners or those just starting out.

Advantages: Quick set up, ease of set up, low cost and good to get started.

Disadvantages: Potential liabilities both tax and legal. Further, the tax situation is complicated and becoming more so, particularly for online merchants once they reach a certain size.

For Americans: Set up a company, obtain an EIN, open a bank account and set up a merchant account. Avoid additional compliance requirements of going offshore.

For Non-Americans: Set up a company, obtain an ITIN, open a bank account and set up a merchant account.

As you can see displayed on the diagram to the right your website is interfacing with a full stack solution. In fact, Paypal makes it very easy for people to accept payments on their website; many vendors just never understand the full concept of how the technology actually processes the customers’ credit card. Even still, this is an oversimplification, but it illustrates an important point and distinction between onshore and offshore credit card processing for your purposes as a vendor.

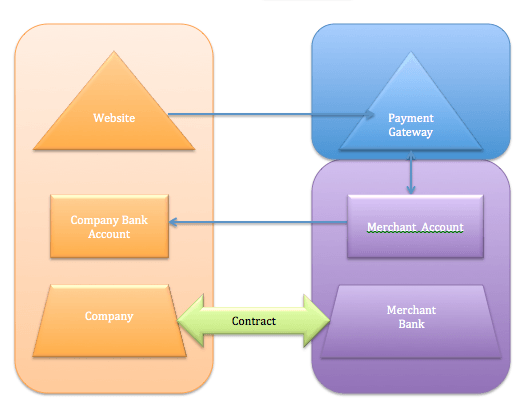

In larger markets, the industry has consolidated and is relatively transparent, meaning very low rates are possible, and you can find a “one-stop-shop” for your payment needs. However, if you are processing risky payments, you have an offshore company or you wish to have more control over the processing, you might need to obtain a merchant account and have a contract directly with a merchant bank (shown in the diagram below in part 3).

The Bottom line: Set up a Wyoming LLC for a quick, easy and inexpensive solution to charge cards for your online business.

Part 2: United Kingdom

Let’s say you want to expand and sell to Europe, you could set up a company, merchant account and have an entirely new setup for this market. Or, you could form a subsidiary. The UK should be the first place you look.

Advantages: Quick setup, ease of setup, low cost and easy to get started.

Disadvantages: Potential liabilities both tax and legal. Many requirements for maintaining compliance, see below.

For Americans: You might look at other options such as Switzerland, Malta or Luxembourg. Unless you are doing a significant turnover, stick with the US market for now, because more complicated setups require professional help and advise. Large businesses such as Amazon (Luxembourg) and Google (through a set up known as a double Irish – Dutch Sandwich) have specialized structures that maximize profits and effectively minimize and avoid taxation. Careful attention is paid to ensure compliance with IRS tax law and other local tax laws.

For Non-Americans: You might look into having a GB subsidiary with a Nevis holding company for example. This setup could potentially allow for tax-free earnings to accrue. However, you should get individual tax advice for any legal setup before taking action. I’m just letting you know it is available and has worked for others…

Compliance: The UK is more complicated and one of the stricter places in terms of setting up a merchant account or selling online. However, the merchant accounts are powerful and can process the European market without having processing errors. The UK is an effective route to gain access to the entire European market in an efficient manner. However, the compliance can be burdensome, for instance, see below for details from this UK government site.

After an order is placed online

You must get in touch with your customer in writing after an order is placed and before the goods have been delivered and ensure the following:

- how and when they can cancel an order and who pays for returning goods

- an address where complaints can be sent

- any guarantees or after-sales services you offer

- conditions for terminating contracts of over 1 year or open-ended contracts

- https://www.gov.uk/online-and-distance-selling-for-businesses/overview

- list the steps involved in a customer placing an order

- acknowledge receipt of any orders electronically as soon as possible

- take reasonable steps to allow customers to correct any errors in their order

- let customers know what languages are available to them

- make sure customers can store and reproduce your terms and conditions, ie these can be downloaded and printed off

- give your email address

- give your VAT number (if your business is registered for VAT)

- give clear prices and delivery costs for your products

Selling within the EU

You must charge VAT to EU customers if you’d do the same for customers in the UK.

You must not charge VAT for customers outside of the EU. Instead, fill out a customs declaration when you ship the products.

Selling outside of the EU

- the customer’s order – including their name, VAT number and delivery address

- internal correspondence

- sales invoices

- advice notes

- packing lists

- commercial transport documents

- details of insurance or freight charges

- bank statements

- consignment notes

There are a number of different requirements and burdens that go along with selling from the UK. You can see that the burden of proof relies pretty heavily upon the seller. However, the EU and the UK do offer a large market of buyers with credit cards at the ready. There are certain structures which can take advantage of this market and potentially provide a tax free setup for the seller while remaining compliant with local laws and regulations.

However…

It still doesn’t beat offshore…

Part 3: Offshore

When dealing with an offshore bank the situation is often quite different from what you might normally be used to. These banks face a number of high-risk clients, and for that reason, need to be stringent during their application and vetting process. This is why it helps dramatically to have an introduction.

However, the merchant bank doesn’t care where you are able to get an account, but just that you have one. In other words, you can get a merchant bank account with almost any offshore bank account. This is a common misconception and oftentimes not understood! Said differently, the merchant bank only needs to be able to transfer money from your merchant account at their bank, to your company account at another bank.

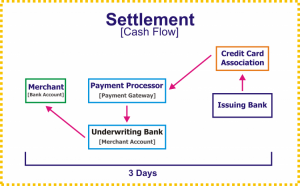

Flow Chart – How it Works

Here you can see a company, the company website and the company bank account. This could be an onshore or offshore company, it doesn’t matter. With the offshore company, you will apply for merchant accounts with merchant banks. These are separate and distinct banking entities which are used to process credit cards.

If the merchant bank accepts your application, they will set you up with a merchant account. Some will help set up a payment gateway, others will allow or require 3rd party integration.

The payment gateway is oftentimes another separate company who provides the front-end and talks to the merchant account through some API.

The customer will land on your website and select a product to buy. From there, they will add items to a cart, and be redirected to a payment gateway (with PCI compliance) which captures the credit card information. The gateway passes this information to a merchant account which processes the actual transaction.

At this point, the visitor can be redirected to a landing page for either a download or will be able to view a receipt for a physical product, as the request is passed to a fulfillment center.

Many time people will utilize a Hong Kong company which is sometimes considered “offshore” in that it is possible to achieve a 0% tax rate, but retains a favorable reputation.

It is possible to find payment processors like Clickbank and PayPal for this jurisdiction, however, the options are oftentimes limiting. Clickbank makes things super easy in exchange for higher fees.

If you can justify an Offshore setup, you should probably have your own merchant account and take greater accountability for one of the most important legs of your business: collecting money from customers.

===============================================================================

Part 4: Higher Risk

There are some websites which banks classify as high risk. Recently platforms like Bitcoin exchanges have been cut out. Other things which may be illegal in one area but legal in another (gambling, pornography, pharma) also tend to classify as extremely high risk. There are certain merchants banks who will deal with these darker industries, usually on an industry specific basis. These merchants also tend to require deep history, and a rolling reserve ratio.

Belize

There are a number of banks in Belize that accept merchants for all types of businesses. You can apply for a merchant account first (usually there is a couple hundred dollar fee associated with the application) and then you will be able to set up a bank account, and receive money into the account. In Belize, (and most offshore merchant accounts) you will need to monitor your chargeback rates. Furthermore, it is important to note that many times there is a rolling reserve.

EcoPayz

EcoCard is very similar to Moneybookers (Skrill) and Neteller.

EcoCard generally absorbs any chargebacks if you can maintain a low chargeback ratio.

Fine print: EcoPayz is a brand name of PSI-Pay Ltd. PSI-Pay Ltd is authorized and regulated by the FCA under the Electronic Money Regulations 2011 (900011) for the issuing of electronic money. PSI-Pay Ltd registered office is at Afon Building, Worthing Road, Horsham, West Sussex, RH12 1TL, England.

EntroPay

EntroPay is a product by Ixaris Ltd, an English-Maltese company and has a 4.95% top-up fee) and merchants.

Fine print: Ixaris Systems Ltd is authorized and regulated by the Financial Conduct Authority under the Payment Service Regulations 2009 for the provision of payment services. (540990). EntroPay VISA cards are issued by Bank of Valletta based in Malta.

Moneta is an e-wallet covering eastern Europe and Russia

Skrill – Is an option for those using offshore banks

Qiwi – Is similar to Moneta, except virtual and plastic pre-paid card for use in Russian speaking countries.

CashU is a voucher type payment system used only throughout the Middle East. They are owned and operated by SOUQ.com

Ticket-Premium Is a French-based, voucher-type system.

OKpay – is an E-wallet type system, that you might want to avoid. The fine print is terrible. Fine Print: Financial Services provided by Mayzus Financial Services Ltd.

(previous name UWC Financial Services Ltd, name changed on 18.03.2013) VG1110, Quijano Chambers, P. O. Box 3159, Road Town, Tortola, British Virgin Islands

Want more?

Digital Currencies are springing up by the thousands. You can explore their current market capitalization here:

Time will tell if new technologies such as Bitcoin will displace current market leaders. The problem is that many people aren’t using this system for payment. Colleague Tim Swanson wrote this interesting piece on coindesk – which showed the overall transaction volume of Bitcoin is quite low. In other words, people are speculating and buying to hold, rather than transact with their bitcoins.

Paypal Killers

Some other options which I think we will see growth in the coming years include Stripe, Peakium and Peakium Spaces, 2C2P, Mergepay, Gumroad. There are a number of interesting companies in the payments space that could disrupt the fragmented, opaque and narrow payments market.

Running a payments company is difficult because people are always trying to steal from you. Either people are processing fake cards, or hacking your backend, performing social engineering, generally trying to cheat you as they assume you have money and may be vulnerable. One needs to look no further than the Mt. Gox collapse. Another reason it is very difficult to run a payments company is that even though the technology can scale nicely, the % of transaction merchants want to give up tends to be low. That means that your economies of scale are good, but it’s difficult to get started. Likely you will need some kind of outside funding. In other words, 3% of $100,000 is not fun – 3% of a $1,000,000,000,000 is.